Running a business does not only equate in earning profits and giving satisfaction to the market. Instead, there is also an inherent obligation to their employees and to the government. That is why Bureau of Internal Revenue (BIR) designed BIR Form 1601-c or Monthly Remittance Return of Income Taxes Withheld on Compensation wherein it helps the employers in fulfilling their statutory responsibility.

What is BIR Form 1601-c?

BIR Form 1601-c is a return filed by an employer/company when they are needed to withhold or remove taxes to the compensation of their employees before the release of payments.

Purpose of BIR Form 1601-C

· To notify the Bureau of Internal Revenue that the business/company has employees.

· To encourage voluntary compliance by providing a convenient way to the taxpayers in withholding their employees’ taxes.

Who needs to file BIR Form 1601-C?

Every company or business who has a workforce or employee/s.

Who is subjected to withholding tax?

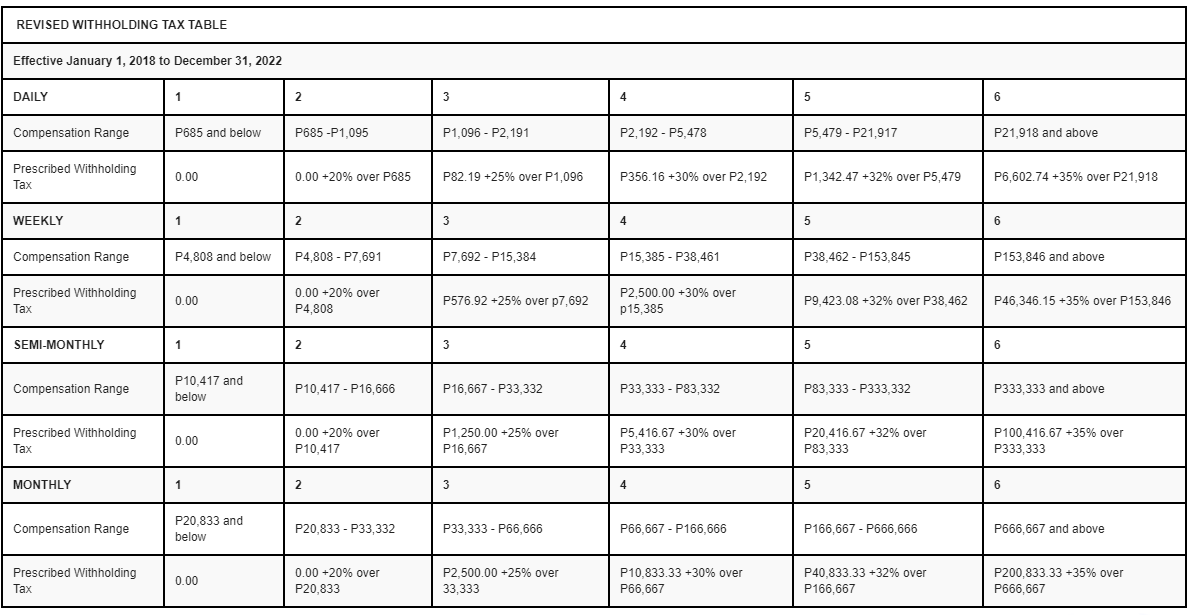

Employee’s salary that exceeds to the monthly minimum wage (Php 20,833.33) or with an annual income above Php 250,000 will be subjected to the creditable withholding tax.

Mode of Filing

· For manual filing, taxpayer is required to visit nearest Authorized Agent Bank of Regional District Office for declaration of taxes.

· For electronic filing, you may visit BIR Official website, then download e-BIR Package or Electronic Filing and Payment System (EFPS) Package

Deadline of filing

The return shall be filed and tax paid on or before the tenth (10th) day of the month following the month in which withholding was made except for taxes withheld for December which shall be filed/paid on or before January 15 of the succeeding year.

Information needed for BIR Form 1601-C

· Total Amount of Compensation

· Non-taxable / Exempt Compensation

a) Compensation of Minimum Wage Earners

b) Other compensations of MWE Employees (Overtime pay, Holiday pay, Hazard pay, Night Differential pay)

c) Statutory Contributions (SSS, HDMF, PAG-IBIG)

d) 13th month pay and de minimis benefits

· Taxable compensation not subject to withholding tax (for employees, other than MWEs, receiving P250,000 & below for the year)

· Total Taxes Withheld for employees’ taxable compensation subject to withholding tax

Computation of Withholding Tax

(Employee’s Compensation – Tax Base) x Percentage

Example:

Juan Cruz, an employee of ABC Company is earning Php 30,000 per month.

His employer, ABC Company has the responsibility to file BIR Form 1601-c every month in order for compliance of withholding tax.

Leave a comment